Retire While You Work® Podcast

Join us as we discuss various topics to help you find the path to viewing money as a means to the true currency, TIME, and learn how to build more memories and experiences.

View All Episodes

Join us as we discuss various topics to help you find the path to viewing money as a means to the true currency, TIME, and learn how to build more memories and experiences.

View All Episodes

A recent conversation with a buddy went like this:

Friend: “I guess now that the yield curve has inverted, I should probably sell my stocks?”

Me: “Why?”

Friend: “Because when the yield curve inverts it means a recession is coming.”

Me: “How so?”

Friend: “Heck, I don’t know, that’s why I’m asking you!”

While I was clearly being obtuse, the point I was making is that while many people read the headlines, few of them may understand the practical application. There has certainly been much talk about the inverted yield curve lately and its predictive abilities regarding recession.

First, the yield curve is simply the relationship between short-term interest rates and long-term interest rates. In a normal environment, shorter rates are lower than longer because a lender wants to be compensated for additional risk of loaning money for a longer period. Additionally, the longer the term of a loan, the more inflation can eat into the returns for the lender. An inverted yield curve occurs when longer interest rates fall below short-term rates, and odd occurrence for sure. In the past, this happened because lenders think economic growth might slow and interest rates may fall even farther. And therein lies its predictive ability of economic weakness.

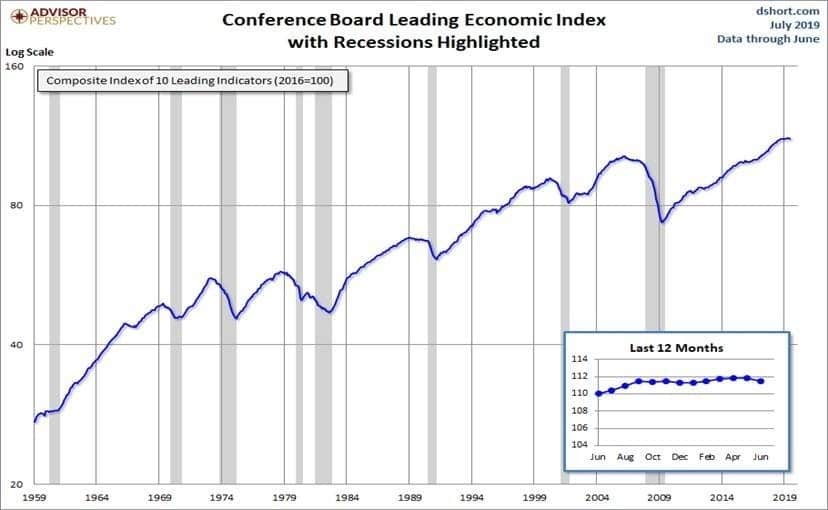

The problem is that the slight inversion that has occurred may be attributed to central bank manipulation and a flood of foreign investment into our bond market – NOT because lenders are scared. Other countries interest rates are extremely low and even negative in many areas of the world (negative interest rates are an even more bizarre economic tool, the merits of which are a debate for another day). This central bank intervention has distorted the yield curve and, in my opinion, reduces its reliability in predicting recession. In addition, the index of leading economic indicators, a commonly-watch barometer of economic activity, has not turned negative commensurate with a recession – see graph below.

(Click to enlarge graph)

Markets have gyrated wildly in August grappling with conflicting data and political headlines and in doing so, have kept valuations from becoming extreme in my opinion. This can be a good thing as the market lets air out of the tire, perhaps a little along the way rather than all at once. On a valuation basis, the market currently trades slightly above its historical valuation based on underlying earnings and folks, markets generally don’t crash from reasonable valuations. They may go through normal corrections as we saw in December, as well as May and now August, but these are normal market adjustments in my opinion and are not worth trying to outguess. As Warren Buffett once said: “I’ve seen more money lost trying to avoid corrections than ever lost during the corrections themselves”.

Even with the declines in May and August, markets are still largely positive, and a balanced portfolio has served many investors well this year. Interest rates and unemployment are low, housing, autos and construction are strong, the consumer is in decent shape, restaurants are full, and lines are long….if this is what a weak economy looks like, I’ll take it. There’s no way to know exactly how long the current economic expansion will last or how much volatility is in store (August and September have historically been two of the most volatile months in the stock market). But a well-known market strategist that I follow closely recently warned that investor sentiment was still very negative and that it is quite possible they may miss out on potential gains should the economy regain traction at year-end. He stated: “Remember, in a bull market many of the surprises are to the upside, not the downside”. Of course, there is no guarantee of such occurrence and markets still have a way of making people eat crow – which is why there’s never been a better time to maintain a diversified portfolio in my humble opinion.

As always, we appreciate your business and urge you to share this with anyone you feel may benefit. We are grateful for all the wonderful referrals you have provided over the years. Until next month, save more, spend less and enjoy life…

The information contained in this letter does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of David Adams. and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Diversification and asset allocation do not ensure a profit or protect against a loss. Holding investments for the long term does not insure a profitable outcome. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance.

Individual investor’s results will vary. Past performance does not guarantee future results. Future investment performance cannot be guaranteed, investment yields will fluctuate with market conditions.

Adams Wealth Partners, LLC is not a registered broker/dealer and is independent of Raymond James Financial Services. Investment advisory services offered through Raymond James Financial Services Advisors, Inc. Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC

Neither Raymond James Financial Services nor any Raymond James Financial Advisor renders advice on tax issues, these matters should be discussed with the appropriate professional.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

The running stock ticker is not a recommendation to buy or sell stocks of the companies pictured.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC, marketed as Adams Wealth Partners. Investment advisory services offered through Raymond James Financial Services Advisors, Inc.Adams Wealth Partners is separately owned and operated and not independently registered as a broker-dealer or investment adviser.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design) and CFP® (with flame design) in the U.S., which it awards to individuals who successfully complete CFP Board's initial and ongoing certification requirements. CFP® holders at Adams Wealth Partners, LLC are: David Adams, Myles Zueger, Carson Odom, and Spencer Provow

CPA holders at Adams Wealth Partners, LLC are: David Adams, Carson Odom, and Christine Kinsley

Please note that all archived content is for informational purposes only. Investment decisions should not be based on the content provided herein. For the most up-to- date statistical information and analysis, please contact your financial professional.

Raymond James financial advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Therefore, a response to a request for information may be delayed. Please note that not all of the investments and services mentioned are available in every state. Investors outside of the United States are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this site. Contact your local Raymond James office for information and availability.

The 2024 Forbes ranking of America’s Top Wealth Management Teams Best-In-State, developed by SHOOK Research, is based on an algorithm of qualitative criteria, mostly gained through telephone and in-person due diligence interviews, and quantitative data. This ranking is based upon the period from 3/31/2022 to 3/31/2023 and was released on 01/09/2024. Advisor teams that are considered must have one advisor with a minimum of seven years of experience, have been in existence as a team for at least one year, have at least 5 team members, and have been nominated by their firm. The algorithm weights factors like revenue trends, assets under management, compliance records, industry experience and those that encompass best practices in their practices and approach to working with clients. Portfolio performance is not a criteria due to varying client objectives and lack of audited data. Out of approximately 10,100 team nominations, 4,100 advisor teams received the award based on thresholds. This ranking is not indicative of an advisor's future performance, is not an endorsement, and may not be representative of individual clients' experience. Neither Raymond James nor any of its Financial Advisors or RIA firms pay a fee in exchange for this award/rating. Raymond James is not affiliated with Forbes or Shook Research, LLC. Please see https://www.forbes.com/lists/wealth-management-teams-best-in-state/ for more info.

Barron’s Top 1,200 Financial Advisors 2023, is based on the period from 09/30/2021 - 09/30/2022 and was released on 03/15/2023. 5630 nominations were received and 1,200 won. Neither Raymond James nor any of its advisors pay a fee in exchange for this award. More:https://www.raymondjames.com/award-disclosures/#2023-barrons-top-1200

Please note that all archived content is for informational purposes only. Investment decisions should not be based on the content provided herein. For the most up-to- date statistical information and analysis, please contact your financial professional.

Raymond James is not affiliation and does not endorse the above-mentioned organizations.

Nashville Wealth Management & Financial Advisors | David Adams CPA, CFP® | Copyright © 2024 | Privacy Notice | Legal Disclosure